Hi everyone,

Just a quick article to discuss a commodity that seemingly out of nowhere has hit the headlines in both the mainstream and the alternative media (for different reasons) - lithium. As most of you will know, lithium is a key industrial metal that is used predominantly in batteries. Today these batteries are used in a whole host of electronics, ensuring lithium will be a key commodity in the (not quite) renewable energy transition.

Although lithium uses vary by location, global end uses were estimated as follows: batteries, 87%; ceramics and glass, 4%; lubricating greases, 2%; air treatment, 1%; continuous casting mold flux powders, 1%; medical, 1%; and other uses, 4%.

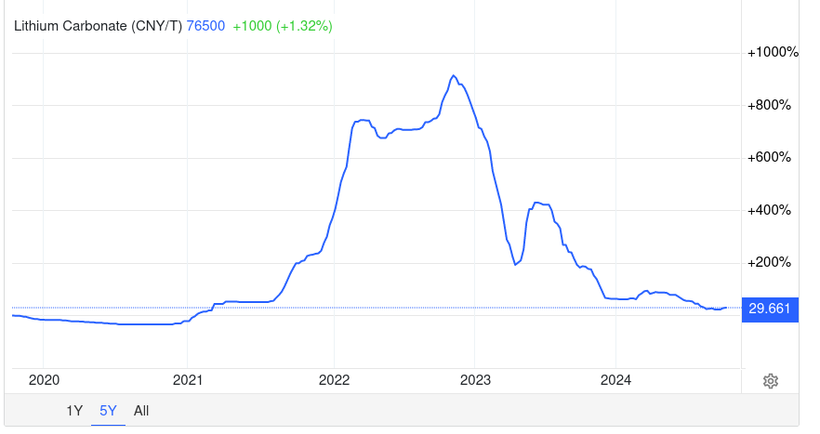

In terms of the price, over the past 3 years lithium has been extremely volatile. After a wild spike in 2022 that saw the price increase almost ten-fold in 18 months to 70,000/ tonne, it then collapsed between 2023 and 2024 all the way back to under 10,000/ tonne. This was largely due to the hyperbolic mainstream media narratives around electronics which went from 'battery revolution and lithium shortages' to 'we have too much lithium!'. The 'experts' estimated this oversupply would take years to resolve. I wasn't so certain about that, so I did my own digging.

Based on my research paired with my outlook on the geopolitical environment, I had a strong feeling that irrespective of the current supply situation, lithium could become one of the most fought over commodities. Firstly, I thought talk over global oversupply was exaggerated and at best only a short term issue. This was based on the projected amount of lithium demand for the world going into 2030. I figured if these projections were even half correct, it wasn't too much lithium the world had to be concerned about, but not enough.

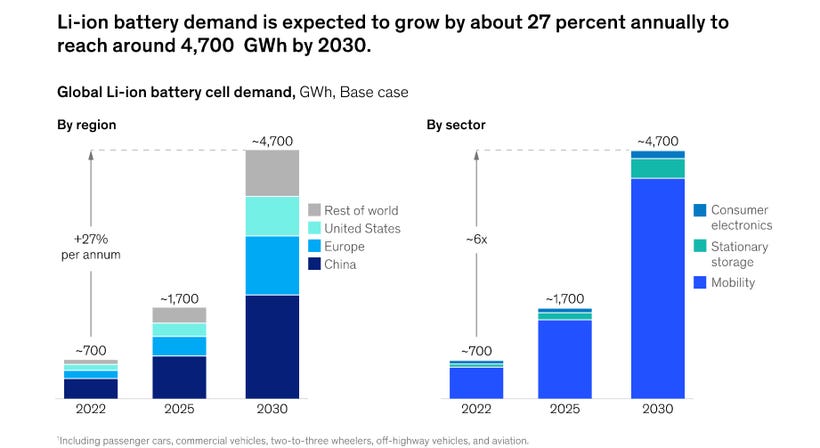

In fact, estimates only grew in terms of just how much lithium the world will require to meet the needs of the energy transition that the global freak class hope to achieve by the end of the 2020's. This was laid out amply in a 2022 report from the McKinsey Institute.

In an earlier publication, a joint 2019 report by McKinsey and the Global Battery Alliance (GBA), and Systemiq, A vision for a sustainable battery value chain in 2030, we projected a market size of 2.6 TWh and yearly growth of 25 percent by 2030. But a 2022 analysis by the McKinsey Battery Insights team projects that the entire lithium-ion (Li-ion) battery chain, from mining through recycling, could grow by over 30 percent annually from 2022 to 2030, when it would reach a value of more than $400 billion and a market size of 4.7 TWh.

Another key part of the lithium narrative that I thought people were overlooking was the effect international conflict and the emerging BRICS bloc was going to have on the supply chains themselves. The ongoing bifurcation between East and West is something I think will dramatically increase between 2025-2030. We are entering the peak of a war cycle and clearly there is a massive fork in the road that we're all now collectively heading towards in terms of relations between superpowers.

This is something I think will effect all commodities ongoing, in ways we're not entirely ready for. Expect to see increased resource hoarding, mine nationalizations, supply chain disruptions (or destructions) and then as a consequence of this, nations increasingly looking for local suppliers over international ones. Especially if those international supplies are mainly in regions of the world that sit on the other side of the East & West divide. Companies that depend on lithium for their product like Tesla are certainly aware of the risks, with Elon Musk even suggesting that Tesla buy a lithium mine of their own in 2022.

I suspected all of this tension behind the future of lithium would lead to volatile prices in commodities like lithium for many years to come, but with a long term trend to the upside. I was correct in one sense, in that lithium was the worst performing industrial metal in 2024, falling 50% this year alone. This was good news for me, as I didn't own any lithium stocks but I felt we were close to the bottom about 4 months back so this is when I made my first tentative steps towards investing in lithium. I bought two companies. One was a large miner called Albermarle.

As of 2020, Albemarle was the largest provider of lithium for electric vehicle batteries in the world. Albemarle, Sociedad Química y Minera, and FMC Corporation collectively produce just over half of the world's lithium and lithium storage products, while just under half is produced by China.

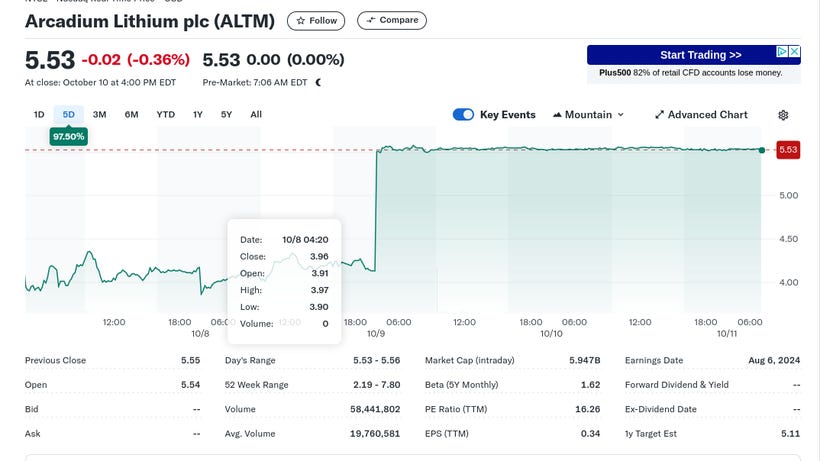

The other company I invested in was called Arcadium Lithium, which is a company that was much less well known. They were formed following the merger of two smaller lithium miners about a year ago and I thought they were being substantially undervalued by the market. In fact, looking at the location of the mines and the synergies that had emerged from the two companies I believed Arcadium was one of the best value lithium plays out there and had big potential. I am a value investor at heart and despite everyone else fleeing the lithium space, I held my nose and invested.

I began buying once the share price fell below $4 a share. I also recommended both companies to my coaching clients in our monthly investor mastermind meeting and mentioned them in our April Newsletter as a buy under $4. Fast forward a few months and just this week Rio Tinto, the worlds second largest miner put in an offer to buy Arcadium for $6.7 billion dollars at a cost of $5.85 a share. The stock is up 97.5% over the past 5 days.

Whilst I had no foreknowledge of the buyout, I am not surprised by it. Arcadium was selling way too cheap and it was only a matter of time before others figured that out. Unlike many lithium plays they were profitable even at the current beat up prices. Many other players in the sector however are deep underwater. Also, they had a great growth profile with plenty of additional production ready to come online in the coming years.

Their balance sheet was strong for a company of its size and also they had a good management team. All things I look for as an investor in mining companies. But they had something else going for them, something I felt wasn't being priced in at all but which I think put another big wind in their sails moving forward. This 'hidden value' was that 11 of their mines/ operations are situation in Western or West allied nations.

Where mines are located is something that I think is going to become extremely relevant in the coming lithium war, which is going to be one of many fronts in a much broader commodities war. It seems like the Rothschild's who are shadow owners of Rio Tinto agreed with me, by buying Arcadium for what the financial press consider a healthy premium.

This was a great outcome for me and my investing group that left most of us up between 45-80% on our investment. The group is made up of people who took group investors coaching with me this year and after coaching is completed we meet monthly for an investors mastermind where we discuss the markets and where the risks and rewards lie. Whilst were on the subject, just quick plug for my group coaching as there is now a waiting list is now in operation for the next round. Come join us as we protect and grow our wealth during these stormy times. Reach out for more info :)

For me the Rio Tinto purchase is a sign that the mega miners see what I see and are going to be far more discerning moving forwards in terms of the location of their operations. One need only look at the consequences of conflict in the middle east on the oil price to see why location matters in a world gone mad. Beyond supply shocks due to conflict resource nationalism is something that is also on the increase, as are mine nationalizations, which is the absolute worst thing that can happen to a miner (and those who invest in them!).

This is something I have been warning about for some time. One of my very first youtube videos was a very crappy low budget white board presentation (that makes me cringe to this day) in which I discuss why the rise of BRICS and their gold/ commodity backed currency is going to completely upend the global supply change for commodities. Let's just stop to consider what a commodity backed currency means for the many companies, mostly Western based, who have mining operations in countries who are lining up to take part and join BRICS.

Whilst in the current FIAT system the Western elites have been more than happy to exploit these nations for their natural wealth, mostly on the cheap, a genuine alternative has now emerged through the BRICS system which is promising them a fairer shake. My guess is they're going to take it. Especially if they have a healthy amount of natural resources. This is actually why the BRICS system is so stunningly subversive. Where it just a gold backed system being proposed, it would never work. The nations of the global south would never join it as most of them have little to no gold reserves. The West however, does.

Commodities on the other hand, well these they have in abundance and the BRICS system will enable them to turn those commodities into a form of money that actually functions like gold. This is because the new currency China and Russia are proposing is being created in such a way that a nation can back their portion of it not just with gold, but with commodities. Meaning if you produce them, you can participate. This in theory would enable these nations to escape the debt-slavery FIAT system of the IMF and the World Bank.

There is just one problem. Whilst many nations in the global south do indeed have commodities in abundance, the vast majority of them are actually under the control of Western corporations who set up shop within their borders. Hmm, rock and a hard place. But for how long? The debt pyramiding of the west cannot go on forever and it appears the end is now drawing near. The global south look on in anticipation, recognizing their time has come.

Case in point, this year we saw Burkina Faso, one of the poorest nations on earth begin nationalizing the gold mines of Western corporations that sit within their country.

Gold is the main metal exported from Burkina Faso. Gold production across West African nations, led by Burkina Faso, Ghana, Mali and the Republic of Guinea, according to Mining Technology’s parent company GlobalData, is expected to reach 11.83 million ounces (moz) in 2024, a 2.6% increase from 2023.

However, production in Mali and Burkina Faso is expected to decline by 5.5% collectively in 2024 due to factors such as lower ore grades, planned reduction and temporary suspension of operating activities.

On Monday (7 October), shares of some of the gold mining companies operating in the West African country, including Endeavour Mining (based in the UK), West African Resources (Australia), Nargold (Russia) and Orezone Gold Corporation (Canada), all dropped significantly.

Many other nations making similar overtures and if a more substantial conflict does emerge going into the latter half of the decade, sides will soon be picked. You go East, or you go West. This I believe will be absolute carnage for the mining sector and as a consequence the global supply chain for essential commodities like lithium. This recent purchase by Rio Tinto is a big clue that we're getting close to this scenario playing out, which is why right now I think there are huge opportunities in gold, silver and commodities. Knowing what you are doing and why is going to be key moving forwards however, which is why in coaching I focus first and foremost on teaching people how to excel at wealth preservation and risk management. It is this what enables us to take advantage of great opportunities like Arcadium Lithium, when they arise.

One final discussion point that I have yet to mention is the recent hurricanes and flooding in the US and how lithium played into them. Which is were things get quite strange, as the company I mentioned earlier Arcadium actually have their US head office in a place called Charlotte. Yes, the same Charlotte that was recently flattened by 'natural' disaster. You have to admit, that is a pretty strange coincidence given who just bought the company out. They themselves don't have a lithium mine in operation there (yet), but both Albemarle and Piedpont Lithium have permitting and projects based in the region.

This is something that leaves a very bad taste in the mouth and it was quickly picked up on in the alternative media. A part of me even thinks that the price crash in lithium over the past year was engineered to enable companies and mines to be bought up on the cheap, but I digress. If you want to learn more about how these weather events play into the lithium war it Monica Perez did a great podcast on this topic this week which is well worth a listen.

GROUP COACHING FOR INVESTORS DISCOUNT

To learn more about group coaching with Mike or join the check out this video.

When it comes to finances, I operate from the principle of DTA...don't trust anyone with your wealth! It's too risky and most advisors or 'experts' are simply not equipped for what we're facing. My ethos has always being that if we want to succeed in protecting and growing our wealth going forward we have to learn those skills for ourselves.

Helping you to achieve that is something I take seriously, which is why I made my coaching in person over zoom. I also offer support for an entire year, with monthly invites to the investors mastermind group where myself and other coaching graduates meet to discuss risks and opportunities. This is certainly not a cookie cutter course with a few pre-made videos, I am there every week to work with you live.

So for anyone who has considered coaching in the past or feels it's time to take control of their own wealth, I am going to be offering a discount to the first 4 people who join us for the next coaching group. If you want to chat about coaching reach out via email or message :)