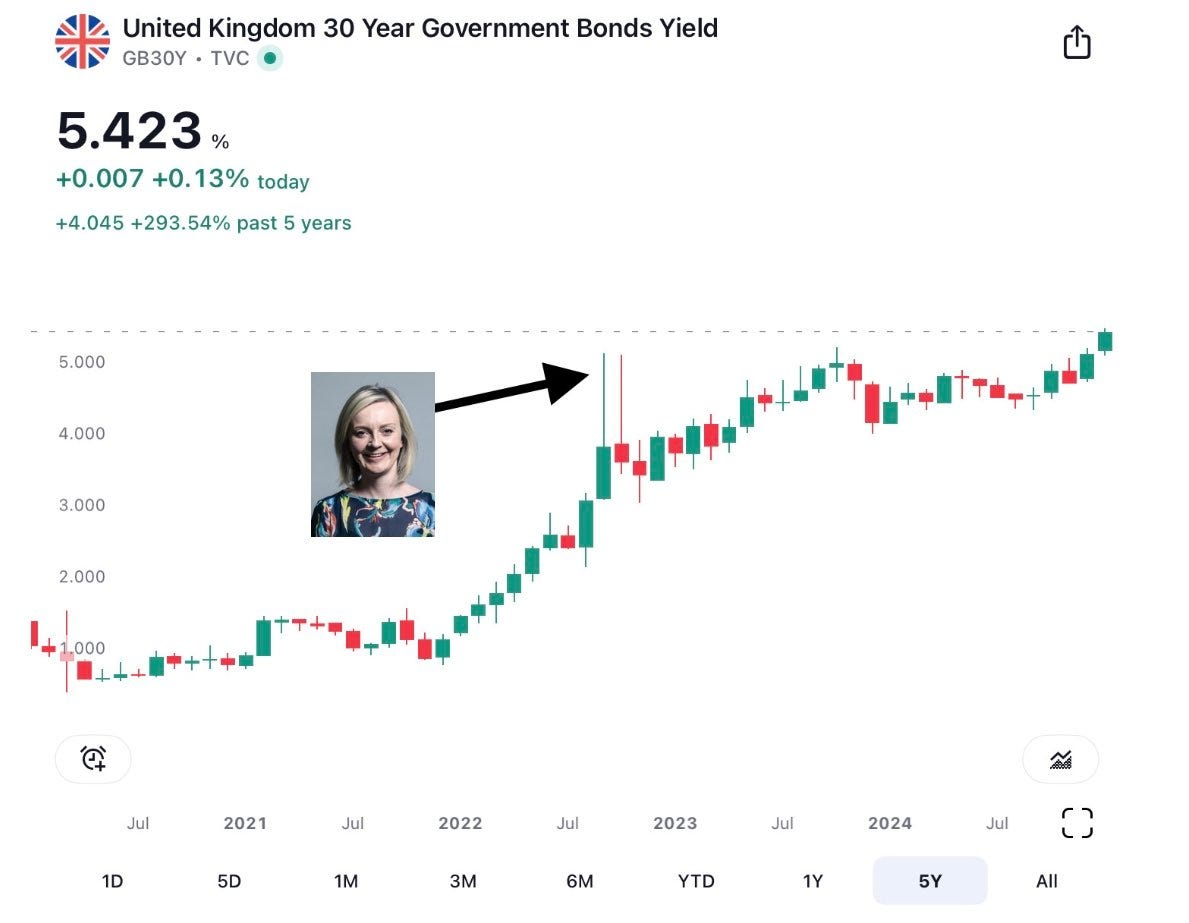

The 2022 LDI crisis in the UK was a critical moment in the series of events pointing to a coming reckoning for the financial system. It revealed an uncomfortable truth...the pensions people had been paying into for decades are destined to be defaulted on. The Bank of England itself acknowledged this in their post-mortem of the crisis—but by then, the average person had already switched over the channel. Keep calm, and carry on.

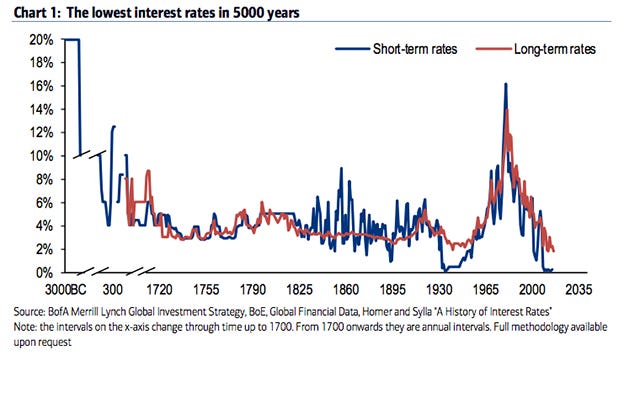

For those of us paying attention, however, it demonstrated the threat of rising bond yields in a post-GFC world. This is something I’ve been warning about ever since the channel began. You simply cannot take bond yields to 5,000-year lows and flood the system with artificial liquidity without shattering the fundamental support pillars of the existing financial system.

In this instance, UK pension funds had increasingly relied on LDI strategies to match their future liabilities with long-term, low-yielding gilts. Low-yielding and long-term are the key parts of the equation here. Because when long-term bond yields spiked dramatically in the wake of a government budget announcement under poor old Liz Truss, the collateral value of these bonds dropped precipitously. To meet margin calls on these derivatives, pension funds were forced to liquidate assets, leading to a collapse in the real value of pensions.